Join Our Groups

TOPIC 5: DEPRECIATION

Several methods are used to compute depreciation. It can be calculated by straight-line method, declining balance method, and Sum-of -the Years'-Digits Method. When choosing a depreciation method,much consideration is given to the matching principle. The main goal is to match the cost of assets to the periods when the assets provide benefits to the business.

Computing Depreciation by the Straight Line

Compute depreciation by the straight line

Straight-Line method is the simplest method used to calculate depreciation of an asset. accountants in favor of this method believe that an asset provides equal benefits over its useful life.

Straight-line Depreciation

The simplest and most commonly used method, straight-line depreciation is calculated by taking the purchase or acquisition price of an asset, subtracting the salvage value (value at which it can be sold once the company no longer needs it) and dividing by the total productive years for which the asset can reasonably be expected to benefit the company (or its useful life).

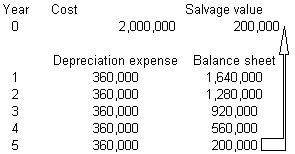

Example 1

Example:

For $2 million, Company ABC purchased a machine that will have an estimated useful life of five years. The company also estimates that in five years, the company will be able to sell it for $200,000 for scrap parts.

| Depreciation Expense = Total Acquisition Cost – Salvage Value / Useful Life |

Straight-line depreciation produces a constant depreciation expense. At the end of the asset's useful life, the asset is accounted for in the balance sheet at its salvage value.

Computing Depreciation by Units of Output

Compute depreciation by Units of output

You have learned that, under straight line method, depreciation is calculated as a function of time. For some assets, depreciation can be direct related to the unit of work it produced. The unit-of-output method is used to calculate depreciation at the same rate for each unit produced. It can measure depreciation in terms of number of hours the asset is used or physical quantities of production.

Unit-of-Production Depreciation

This method provides for depreciation by means of a fixed rate per unit of production. Under this method, one must first determine the cost per one production unit and then multiply that cost per unit with the total number of units the company produced within an accounting period to determine its depreciation expense.

| Depreciation Expense = Total Acquisition Cost - Salvage Value / Estimated Total Units |

Estimated total units = the total units this machine can produce over its lifetime

Depreciation expense = depreciation per unit * number of units produced during an accounting period

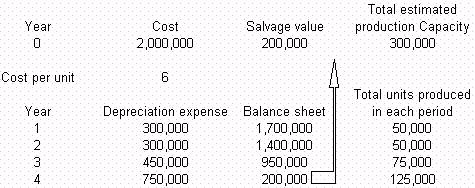

Example 2

Example:

Company ABC purchased a machine for $2 million that can produce 300,000 products over its useful life. The company estimates that this machine has a salvage value of $200,000.

Unit-of-production depreciation produces a variable depreciation expense and is more reflective of production-to-cost (see matching principle).

At the end of its useful life, the asset's accumulated depreciation is equal to its total cost minus its salvage value. Furthermore, its accumulated production units equal the total estimated production capacity. One of the drawbacks of this method is that if the units of products decrease (due to slowing demand for the product, for example), the depreciation expense also decreases. This results in an overstatement of reported income and asset value.

Computing Depreciation by Declining Balance

Compute depreciation by Declining balance

The declining- balance method is an accelerated method of depreciation. It allocates greater amount of depreciation to an asset's earl years of useful life.

Reducing Balance Depreciation Method

Reducing Balance Method charges depreciation at a higher rate in the earlier years of an asset. The amount of depreciation reduces as the life of the asset progresses. Depreciation under reducing balance method may be calculated as follows:

Depreciation per annum = (Net Book Value - Residual Value) x Rate%

Where:

- Net Book Value is the asset's net value at the start of an accounting period. It is calculated by deducting the accumulated (total) depreciation from the cost of the fixed asset.

- Residual Value is the estimated scrap value at the end of the useful life of the asset. As the residual value is expected to be recovered at the end of an asset's useful life, there is no need to charge the portion of cost equaling the residual value.

- Rate of depreciation is defined according to the estimated pattern of an asset's use over its life term.

Example 3

Example:

An asset has a useful life of 3 years.

Cost of the asset is $2,000.

Residual Value is $500.

Rate of depreciation is 50%.

Depreciation expense for the three years will be as follows:

| NBV | R.V | Rate | Depreciation | Accumulated Depreciation | ||||

| Year1: | (2000 | - | 500) | x | 50% | = | 750 | 750 |

| Year2: | (1250 | - | 500) | x | 50% | = | 375 | 1125 |

| Year3: | (875 | - | 500) | x | 50% | = | 375* | 1500 |

*Under reducing balance method, depreciation for the last year of the asset's useful life is the difference between net book value at the start of the period and the estimated residual value. This is to ensure that depreciation is charged in full.

As you can see from the above example, depreciation expense under reducing balance method progressively declines over the asset's useful life.

Reducing Balance Method is appropriate where an asset has a higher utility in the earlier years of its life. Computer equipment for instance has better functionality in its early years. Computer equipment also becomes obsolete in a span of few years due to technological developments. Using reducing balance method to depreciate computer equipment would ensure that higher depreciation is charged in the earlier years of its operation.

Example 4

Example

|

Depreciation to be expensed for the three years will be:

| NBV | R.V | Rate | Depreciation | Accumalated Depreciation | ||||

| Year1: | (4,000 | - | 300) | x | 50% | = | 1,850 | 1,850 |

| Year2: | (2,150 | - | 300) | x | 50% | = | 925 | 2,775 |

| Year3: | (1,225 | - | 300) | x | 50% | = | 925* | 3,700 |

Computing Depreciation by Sum of the Years Digits

Compute depreciation by Sum of the years digits

Sum-of-Year Method:

| Depreciation In Year i = ((n-i+1) / n!) * (total acquisition cost - salvage value) |

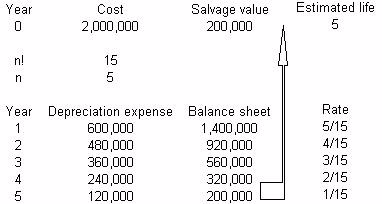

Example 5

Example:

For $2 million, Company ABC purchased a machine that will have an estimated useful life of five years. The company also estimates that in five years, the company will be able to sell it for $200,000 for scrap parts. n! = 1+2+3+4+5 = 15 n = 5

The sum-of-year depreciation method produces a variable depreciation expense. At the end of the useful life of the asset, its accumulated depreciation is equal to the accumulated depreciation under the straight-line depreciation.

Computing Depreciation by Revaluation

Compute depreciation by Revaluation

Under this method the fixed assets are valued at the end of each accounting period. The difference between the value at the beginning of the period and the value at the end of the period represents the depreciation value which is charged against the profit and loss account. This method is used in case of assets like loose tools, packages, Farmers’ livestock etc.

Formula for Calculating:Depreciation = Value of asset at the end – Value of asset at the beginning + Any new purchases

Example 6

A firm had purchased loose tools costing $ 62500 on 1st april 2000. The tools were independent valued at the end of every year and the values placed on them were as under :

- 31st Dec. 2000 $ 60,000

- 31st Dec. 2001 $ 50,000

- 31st Dec. 2002 $ 42,500

- 31st Dec. 2003 $ 32,500

Find out the Amount of Depreciation for each year.

Solution

| AnnualDepreciation Formula=Value at the Beginning-Estimated Value at the End | |||

| Year | Value at the Beginning | Estimated Value at the End | AnnualDepreciation |

| 2000 | 62500 | 60000 | 2500 |

| 2001 | 60000 | 50000 | 10000 |

| 2002 | 50000 | 42500 | 7500 |

| 2003 | 42500 | 32500 | 10000 |

Computing Depreciation by Double Declining Balance

Compute depreciation by Double declining balance

The double declining balance method is an accelerated form of depreciation under which the vast majority of the depreciation associated with a fixed asset is recognized during the first few years of its useful life. This approach is reasonable under either of the following two circumstances:

- When the utility of an asset is being consumed at a more rapid rate during the early part of its useful life; or

- When the intent is to recognize more expense now, thereby shifting profit recognition further into the future (which may be of use for deferring income taxes).

However, this method is more difficult to calculate than the more traditionalstraight-line methodof depreciation. Also, most assets are utilized at a consistent rate over their useful lives, which does not reflect the rapid rate of depreciation resulting from this method. Further, this approach results in the skewing of profitability results into future periods, which makes it more difficult to ascertain the true operational profitability of asset-intensive businesses.

To calculate depreciation under the double declining method, multiply the book value at the beginning of the fiscal year by a multiple of the straight-line rate of depreciation. Thedouble declining balance formula is:

Double-declining balance (ceases when the book value = the estimated salvage value)

2 × Straight-line depreciation rate × Book value at the beginning of the year

A variation on this method is the 150% declining balance method, which substitutes 1.5 for the 2.0 figure used in the calculation. The 150% method does not result in as rapid a rate of depreciation at the double declining method.

Example 7

ABC Company purchases a machine for $100,000. It has an estimated salvage value of $10,000 and a useful life of five years. The double declining balance depreciation calculation is:

| Year | Net book value,beginning of year | Double-declining balance depreciation computed as 2 × SLrate × beginning NBV | Net book value,end of year | |

| 1 | $100,000 | $40,000 | $60,000 | |

| 2 | 60,000 | 24,000 | 36,000 | |

| 3 | 36,000 | 14,400 | 21,600 | |

| 4 | 21,600 | 8,640 | 12,960 | |

| 5 | 12,960 | 2,960 | 10,000 salvage value | |

| Total | $90,000 | |||

The Asset Account, the Provision for Depreciation Account as Balance Sheet Extracts

Show the asset account, the provision for depreciation account as balance sheet extracts

Double entry involved in recoding depreciation may be summarized as follows:

| Debit | Depreciation Expense (Income Statement) |

| Credit | Accumulated Depreciation (Balance Sheet) |

Every accounting period, depreciation of asset charged during the year is credited to the Accumulated Depreciation account until the asset is disposed. Accumulated depreciation is subtracted from the asset's cost to arrive at the net book value that appears on the face of the balance sheet. Using the last example, following double entries will be recorded in respect of depreciation:

| Depreciation Expense Account | |||||

| Debit | $ | Credit | $ | ||

| 2001 | Accumulated Depreciation | 333.3 | 2001 | Income Statement | 333.3 |

| 2002 | Accumulated Depreciation | 333.3 | 2002 | Income Statement | 333.3 |

| 2003 | Accumulated Depreciation | 333.4 | 2003 | Income Statement | 333.4 |

| Accumulated Depreciation Account | |||||

| Debit | $ | Credit | $ | ||

| 2001 | Balance c/d | 333.3 | 2001 | Depreciation Expense | 333.3 |

| 333.3 | 333.3 | ||||

| 2002 | Balance c/d | 666.6 | 2002 | Balance b/d | 333.3 |

| 2002 | Depreciation Expense | 333.3 | |||

| 666.6 | 666.6 | ||||

| 2003 | Balance c/d | 1000 | 2003 | Balance b/d | 666.6 |

| 2003 | Depreciation Expense | 333.4 | |||

| 1000 | 1000 | ||||

An asset Disposal Account and Extracts from the Balance Sheet

Write up an asset disposal account and extracts from the balance sheet

A disposal account is a gain or loss account that appears in the income statement, and in which is recorded the difference between the disposal proceeds and the net carrying amount of the fixed asset being disposed of. The account is usually labeled "Gain/Loss on Asset Disposal."

The journal entry for such a transaction is to debit the disposal account for the net difference between the original asset cost and any accumulated depreciation (if any), while reversing the balances in the fixed asset account and the accumulated depreciation account. If there are proceeds from the sale, they are also recorded in this account. Thus, the line items in the entry are:

- Debit the accumulated depreciation account to reverse the cumulative amount of depreciation already recorded for the asset, and credit the disposal account

- Debit the cash account for any proceeds from the sale, and credit the disposal account

- Debit the disposal account if there is a loss on disposal

- Credit the fixed asset account to reverse the original cost of the asset, and debit the disposal account

- Credit the disposal account if there is a gain on disposal

It is also possible to accumulate the offsetting debits and credits associated with the elimination of an asset and related accumulated depreciation, as well as any cash received, in a temporary disposal account, and then transfer the net balance in this account to a "gain/loss on asset disposal" account. However, this is a lengthier approach that is not appreciably more transparent and somewhat less efficient than treating the disposal account as a gain or loss account itself, and so is not recommended.

Example 8

The following journal entry shows a typical transaction where a fixed asset is being eliminated. The asset has an original cost of $10,000 and accumulated depreciation of $8,000. We want to completely eliminate it from the accounting records, so we credit the asset account for $10,000, debit the accumulated depreciation account for $8,000, and debit the disposal account for $2,000 (which is a loss).

| Debit | Credit | |

| Accumulated depreciation | 8,000 | |

| Loss on asset disposal | 2,000 | |

| Asset | 10,000 |

If the company had instead sold off the asset for $3,000, this would generate a net gain of $1,000, which is recorded with the following entry:

| Debit | Credit | |

| Cash | 3,000 | |

| Accumulated depreciation | 8,000 | |

| Asset | 10,000 | |

| Gain on asset disposal | 1,000 |

Journal Entries to Record Depreciation on Fixed Asset

Show journal entries to record depreciation on fixed asset

Depreciation Journal Entries

When you record depreciation, it is a debit to the Depreciation Expense account, and a credit to the Accumulated Depreciation account. The Accumulated Depreciation account is a contra account, which means that it appears on the balance sheet as a deduction from the original purchase price of an asset.

Once you dispose of an asset, you credit the Fixed Asset account in which the asset was originally recorded, and debit the Accumulated Depreciation account, thereby flushing the asset out of the balance sheet. If an asset was not fully depreciated at the time of its disposal, it will also be necessary to record a loss on undercoated portion. This loss will be reduced by any proceeds from sale of the asset.

Other Depreciation Issues

Depreciation has nothing to do with the market value of a fixed asset, which may vary considerably from the net cost of the asset at any given time.

Depreciation is a major issue in the calculation of a company's cash flows, because it is included in the calculation of net income, but does not involve any cash flow. Thus, a cash flow analysis calls for the inclusion of net income, with an add-back for any depreciation recognized as expense during the period.

Disposal of Fixed Assets Journal Entry – Write Off

| Account | Debit | Credit |

|---|---|---|

| Fixed Assets | 9,000 | |

| Accumulated Depreciation | 6,000 | |

| Disposal of Fixed Assets Account | 3,000 | |

| Total | 9,000 | 9,000 |

The disposal of fixed assets account is an income statement account and is being used to hold all gains, losses, and write offs of fixed assets as they are disposed of. The account is sometimes called the disposal account, gains/losses on disposal account, or sales of assets account. In this case the amount is a debit representing a loss to the business.

Methods of Providing Depreciation Employed

Identify methods of providing depreciation employed

The following are the various methods for providing depreciation:

- Straight Line or Fixed Percentage on Original Cost or Fixed Installment Method.

- Written Down Value or Fixed Percentage on Diminishing Balance or Reducing Installment Method.

- Insurance Policy Method.

- Sum of the Digits Method.

- Revaluation Method.

- Depletion Method.

- Machine Hour Rate Method.

Straight Line Method

Under this method, a fixed percentage of original cost is written off the asset every year. Thus, if an asset costs Rs.20,000 and 10 percent depreciation were considered adequate, Rs.2,000 would be written off every year. The amount to be written off every year is arrived at as under:

= ( Cost – Estimated Scrap Value ) / Estimated Life

The period for which the asset is used in a particular year should also be taken into account. This method is simple in calculation and also in such a case, the charge to the Profit and Loss Account is uniform every year. This method is useful when the service rendered by the asset is uniform from year to year. It is desirable, when this method is in use, to estimate the amount to be spent by way of repairs during the whole life of the asset and provide for repairs each year at the average actual repairs.

Written Down Value Method

Under this method, the rate or percentage of depreciation is fixed, but it applies to the value at which the asset stands in the books in the beginning of the year. In other words, under this method, a fixed percentage is written off every year on the reduced balance of the asset. Thus, the percentage of depreciation is not applied to the original cost but only to the balance, which remains after charging depreciation in the beginning of a year. The percentage of depreciation remains fixed for all the years of the working life of an asset but the actual amount of depreciation written off every year goes on decreasing with the reduction in the value of the asset.

Insurance Policy Method or Capital Redemption Policy Method

Under this method the business takes a policy from an insurance company. The amount of the policy is such that it is sufficient to replace the asset when it is worn out. Cash, which is equal to the amount of depreciation, is paid by way of premium every year. The amount goes on accumulating with the insurance company at a certain rate of interest and is paid back to the insured at the maturity of the policy. The amount so made available by the insurance company is used for purchasing a new asset. This method to a great extent is similar to sinking fund method, but no doubt the procedure is a little different. In this method, instead of buying securities, the insurance policy is taken and premium is paid every year. Company, that receives premium, allows a small interest on compound basis.

This method is a more suitable device for ensuring the availability of cash to replace the asset. The advantage under this system is that the company need not worry whether the investments as under the Depreciation Fund Method, will be sold at best prices or not.

If an insurance policy is taken, it serves two purposes. Firstly, it insures the asset. Secondly, the insurance company will pay the stipulated amount to enable the company to replace assets. This method is more expensive as the insurance company has to keep its margin of profits. It is suitable for losses where the life of the asset is definitely known. It yields a very low rate of interest. It makes no adjustments for price-level changes.

Sum of the Digits Method

Under this method, amount of the depreciation to be written off each year is calculated by the following formula: = Remaining Life of the Asset (including the Current Year) / Sum of all the Digits of the Life of the Asset in Years x Cost of the Asset

Suppose the life of an asset costing Rs.50,000 is 10 years. The sum of all the digits from 1 to 10 comes to 55 i.e., 10+9+8+7+6+5+4+3+2+I = 55. The depreciation to be provided in the first year will be:

= 10 / 55 x 50,000 or Rs.9,091

In the second year, it will be:

9 /55 x 50,000 or Rs.8,181

This method is similar to the Written Down Value Method described earlier.

Revaluation Method

This method is used only in case of small items like cattle (Livestock), or loose tools where it may be too much to maintain an account of each single item. The amount of depreciation to be written off is determined by comparing the value at the end of the year (valuation being done by some one having expert knowledge of the valuation of the asset) with the value in the beginning.

Suppose on 1st April 2,007 the value of loose tools was Rs.10,000 and during the year Rs.30,000 worth of tools were purchased. Now if at the end of the year, the loose tools are considered to be worth only Rs.25,000 the depreciation comes to Rs.15,000 i.e. Rs.10,000+ Rs.30,000 – Rs.25,000.

Depletion Method

The depletion method is used in case of mines, quarries, etc., where an estimate of total quantity of output likely to be available should be available. Depreciation is calculated per ton of output.

For example, if a mine is purchased for Rs.20,00,000 and it is estimated that the total quantity of mineral in the mine is 5,00,000 ton, the depreciation per ton of output comes to = 20,00,000 / 5,00,000 = Rs. 4.

If the output in the first year is 30,000 then the depreciation will be 30,000 x Rs.4 = Rs. 1,20,000, in the second year, the output may be 50,000 ton; the depreciation to be written off will be Rs.2,00,000 i.e., 50,000 x Rs.4.

Machine Hour Rate Method

This is more or less like the depreciation method. Instead of the usual method of estimating the life of a machine in years, it is estimated in hours. Then, an accurate record is kept recording the number of hours each machine is run and depreciation is calculated accordingly.

For example, the effective life of a machine may be 30,000 hours. If the cost of the machine is Rs.4,50,000, the hourly depreciation is

= 4,50,000 / 30,000 = Rs. 15.

The depreciation for a particular year during which the machine runs for 2,500 hours will be 2,500 x Rs.15 = Rs.37,500.

EmoticonEmoticon