Join Our Groups

TOPIC 6: BAD DEBTS

Suppose that you are the owner of a business and you owe someone. What will you do if the credited customer will not be able ton pay back the company's debt? In this concept, I will tell you what to do when that issue happen.When the owner of a business become aware that a customer who has been credited will not be able to pay the amount outstanding, it is very important to take an action and the amount due is written off. The account of the credit costumer will be closed and the profit will be reduced. The bad debt account is an expense account.

The Bad Depts Account

Show the bad debts account

After realizing that there is bad debt, the next stage is to prepare bad dept account as an expense account. The account will be closed and bad debt for the year will be transferred to the income statement.See the sample of bad debt account below

What are bad debts?

Bad debt is usually a product of the debtor going into bankruptcymay also occur when the creditor's cost of pursuing the debt collection activities is more than the amount of the debt. Once a debt is considered bad, the business may be able to write it off as an expense on its income tax return. Due to that a credited customer fail to fulfill his/her obligation to pay the company back.

The bad debts associated with accounts receivable is reported on the income statement as Bad Debts Expense. They affect the company's credit policy.

When the allowance method is used, the journal entry to Bad Debts Expense will include a credit to Allowance for Doubtful Accounts, a contra account and valuation account to the asset Accounts Receivable. The allowance method anticipates the losses and therefore requires the use of estimates.

Under the direct write-off method, the Allowance for Doubtful Accounts is not used. Rather, Bad Debts Expense will be debited when an account receivable is actually written off. The credit in this entry will be to the asset Accounts Receivable.

Accounting entry required to write off a bad debt is as follows:

| Debit | Bad Debt Expense |

| Credit | Receivable |

The credit entry reduces the receivable balance to nil as no amount is expected to be recovered from the receivable. The debit entry has the effect of cancelling the impact on profit of the sales that were previously recognized in the income statement.

Example 1

Example

ABC LTD sells goods to DEF LTD for $500 on credit. ABC LTD subsequently finds out that DEF LTD is being liquidated and therefore the prospects of recovering its dues are very low.

ABC LTD should write off the receivable from DEF LTD in view of the circumstances. The double entry will be recorded as follows:

| $ | $ | ||

| Debit | Bad Debt Expense | 500 | |

| Credit | DEF LTD (Receivable) | 500 | |

Bad Debt Recovered

Occasionally, a bad debt previously written off may subsequently settle its debt in full or in part. In such case, it will be necessary to cancel the effect of bad debt expense previously recognized up to the amount settlement.

Example 2

Example

ABC LTD sells goods to DEF LTD for $500 on credit. ABC LTD subsequently finds out that DEF LTD is being liquidated and therefore the prospects of recovering its dues are very low. ABC LTD therefore writes off the receivable from its books. However, the administrator appointed to oversee the liquidation of DEF LTD instructs the company to pay $300 to ABC LTD in full settlement of its dues.

As $300 of the bad debt has been recovered, it is necessary to cancel the effect of previously recognized bad debt expense up to this amount. The accounting entry will therefore be as follows:

| $ | $ | ||

| Debit | Cash | 300 | |

| Credit | Bad Debt Recovered (Income) | 300 | |

- See more at: http://accounting-simplified.com/accounting-for-bad-debts.html#sthash.6wuDrJGR.dpuf

Provision for Bad Debts Account

The provision for bad debts account

The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. It is identical to the allowance for doubtful accounts. The provision is used under accrual basis accounting, so that an expense is recognized for probable bad debts as soon as invoices are issued to customers, rather than waiting several months to find out exactly which invoices turned out to be uncollectible. Thus, the net impact of the provision for doubtful debts is to accelerate the recognition of bad debts into earlier reporting periods.

A business typically estimates the amount of bad debt based on historical experience, and charges this amount to expense with a debit to the bad debt expense account (which appears in the income statement) and a credit to the provision for doubtful debts account (which appears in the balance sheet). The organization should make this entry in the same period when it bills a customer, so that revenues are matched with all applicable expenses (as per the matching principle).

The provision for doubtful debts is an accounts receivable contra account, so it should always have a credit balance, and is listed in the balance sheet directly below the accounts receivable line item. The two line items can be combined for reporting purposes to arrive at a net receivables figure.

Later, when you identify a specific customer invoice that is not going to be paid, eliminate it against the provision for doubtful debts. This can be done with a journal entry that debits the provision for doubtful debts and credits the accounts receivable account; this merely nets out two accounts within the balance sheet, and has no impact on the income statement. If you are using accounting software, create a credit memo in the amount of the unpaid invoice, which creates the same journal entry for you.

It is highly unlikely that the provision for doubtful debts will always exactly match the amount of invoices that are actually unpaid, since it is only an estimate. Thus, you will need to adjust the balance in this account over time to bring it into closer alignment with the ongoing best estimate of bad debts. This can involve an additional charge to the bad debt expense account (if the provision appears to initially be too low) or a reduction in the expense (if the provision appears to be too high).

Example 3

Example

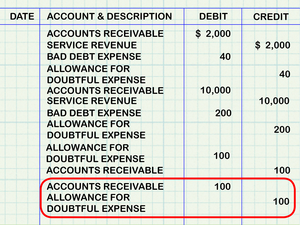

ABC LTD has trade receivable of worth $50,000 as at 31 December 2010. XYZ LTD, a receivable owing $10,000 to ABC LTD at the year end, has been recently been wound up. Consequently, ABC LTD does not expect to recover the amount due from XYZ LTD. Based on past experience, ABC LTD estimates that 5% of its receivables will default. Allowance for doubtful debts on 31 December 2009 was $1500.

ABC LTD must write off the $10,000 receivable from XYZ LTD as bad debt. Accounting entry to record the bad debt will be as follows:

| $ | $ | ||

| Debit | Bad Debt Expense | 10,000 | |

| Credit | XYZ LTD (Receivable) | 10,000 | |

A general allowance of $2,000 [( 50,000-10,000) x 5%] must be made. As a general allowance of $1500 has already been created, only $500 additional allowance must be charged to the income statement:

| $ | $ | ||

| Debit | Allowance for Doubtful Debts (Expense) | 500 | |

| Credit | Allowance for Doubtful Debts (Balance Sheet) | 500 | |

Note that $10,000 in respect of receivable from XYZ LTD has been excluded from the calculation of the general allowance as it has already been written off in full:

| Bad Debt Expense | |||

| Debit | $ | Credit | $ |

| XYZ LTD (Receivable) | 10,000 | Income Statement | 10,000 |

| 10,000 | 10,000 | ||

| XYZ LTD Receivable | |||

| Debit | $ | Credit | $ |

| Sales | 10,000 | Bad Debt Expense | 10,000 |

| 10,000 | 10,000 | ||

| Allowance for Doubtful Debts | |||

| Debit | $ | Credit | $ |

| Balance c/d | 2,000 | Balance b/d | 1,500 |

| Income Statement | 500 | ||

| 2,000 | 2,000 | ||

Preparation of a Computation of the Amount to be Shown as Trade Debtors in the Company Balance Sheet

Prepare a computation of the amount to be shown as Trade debtors in the company balance sheet

The bad debts after trial balance, provision for doubtful debts and provision for discount on debtors will appear in the balance sheet as

| Debtors | xxxx |

| Minus: Bad debts | xxxx |

| Minus: Provision for doubtful debts | xxxx |

| Minus: Provision for discount on debtors | xxxx |

Preparation of a Provision for Discounts on Debtors

Prepare a provision for discounts on debtors

Provision for discount on debtors

In business world a lot of sales transactions happen on credit, i.e. after a specified period of time. In this scenario, there are two main types of discounts allowed to customers. One is trade discount and the other is a cash discount.

Now, after anticipating the amount of cash discount allowable to debtors, a separate “provision for discount on debtors account” is opened and it is very similar to the “provision for doubtful debts account”. The only difference between the two is that provision for discount is calculated on the debtors’ balance after deducting the provision for doubtful debts.

Journal Entry for Creating a Provision on Discount on Debtors

| Profit & Loss A/C | Debit |

| To Provision for Discount on Debtors A/C | Credit |

- If a provision for discount on debtors exists at the time of providing discount, then write off the discount from that provision.

- A new provision should then be calculated to the extent of bringing the existing provision to thenew figure. Ajournal entry would include debiting P&L account and crediting provision for discount on debtors.

- If new provision required is lower than the provision already existent, then we need to transfer the difference to P&L account. In this case, the journal entry would be reverse of what is mentioned in the previous point.

EmoticonEmoticon