Join Our Groups

TOPIC 5: DEPARTMENTAL ACCOUNTS

The Trading Account for a Departmental Store

Draw up the trading account for a departmental store

Introduction:

Departmental Accounts are accounts relating to the several departments or sections of a business drawn up with a view to ascertaining their individual performances. A business may have a number of departments each dealing in a different type of goods. For instance, Departmental Store is an example of large scale trading by a retail trader.

In order to carryout business more efficiently, a businessman divides his store into many sections, each section is called a Department. In order to ascertain the profit or loss made by each department, it is desirable to prepare separate Trading and Profit and Loss Account for each department.

The preparation of such Trading and Profit and Loss Account separately for each department enables to compare the results of trading activities; in brief:

- It enables to compare the performance of one department with that of another and to measure the progress of the department itself by comparing year-wise performance.

- It enables to measure the profitability of each department. In the absence of departmental accounting, if there is a loss, the businessman thinks that the whole business is at loss. Thus he may stop the business and may start a new business, because he is unable to understand the performance of each department. But, by preparing departmental accounts separately, the contribution of profit made by each department can be known. Thus a good profit- making department can be developed and the department which gives small margin of profit or no profit can be closed down. It is also possible to check the profit of a department, not to be eaten away by the department which makes no profit.

- It helps in formulating new policies and to adopt new and latest techniques in the departments, thereby further profitability of the department can be expected.

- Departmental Managers of the profit-making department can be encouraged by adopting a method of commission on the basis of departmental profit. This step will further boost the profit-making department.

Accounting Procedure:

There are two methods of keeping departmental accounts:

- Independent Basis: In this method, accounts of each department are maintained separately. Each department prepares Trading and Profit and Loss Account. Finally, the profit or loss of each department is transferred to the (General) Profit and Loss Account for all the departments. The independent departmental book-keeping is an expensive one.

- Columnar Basis: In this method, there is a single set of books. All accounts of all the departments are maintained together, but in a columnar or tabular form. In order to enable the preparation of departmental trading and profit and loss accounts, various subsidiary books, such as purchases, sales, returns books, are prepared in a columnar form and this shows the record, in detail, for each department.

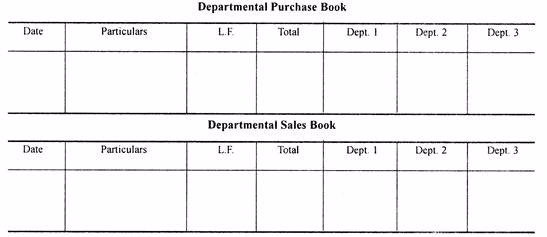

The following is the specimen of a purchase book and a sales book:

The same pattern of rulings may be followed in case of other subsidiary books.

The Overheads Expenses to Department

Apportion the overheads expenses to department

Apportionment of overhead costs means to divide total cost of overhead among different departments or branches or cost centers of a company. We need the steps of apportionment of overhead costs when there are many departments or cost centers of any company because when we know the overhead cost of each department, we can find the total cost of department. With this, we can compare the revenue of each department with their total cost. After this, we can take many decisions relating to particular department.

The Methods Used in Apportioning Overhead Expenses

Explain the methods used in apportioning overhead expenses

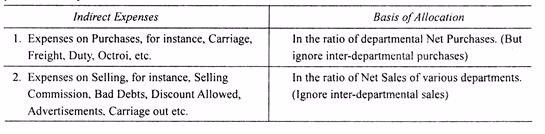

The determination of a suitable basis is of primary importance and the following principles are useful guides to a cost accountant:

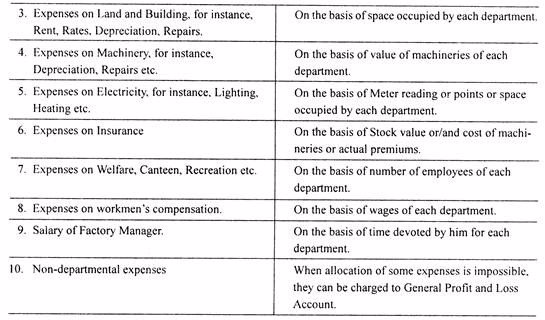

- Service or Use or Benefit Derived:If the service rendered by a particular item of expense to different departments can be measured, overhead can be conveniently apportioned on this basis. Thus, the cost of maintenance may be apportioned to different departments on the basis of machine hours or capital value of the machines, rent charges to be distributed according to the floor space occupied by each department.

- Ability to Pay Method:Under this method, overhead should be distributed in proportion to the sales ability, income or profitability of the departments, territories, basis of products etc. Thus, jobs or products making higher profits take a higher share of the overhead expenses. This method is inequitable and is not generally advisable to relieve inefficient units at the cost of efficient units.

- Efficiency Method:Under this method, the apportionment of expenses is made on the basis of production targets. If the target is exceeded, the unit cost reduces indicating a more than average efficiency. If the target is not achieved, the unit cost goes up, disclosing thereby the inefficiency of the department.

- Survey Method:In certain cases it may not be possible to measure exactly the extent of benefit wick the various departments receive as this may vary from period to period, a survey is made of the various factors involved and the share of overhead costs to be borne by each cost centre is determined.Thus, the salaries of foreman serving two departments can be apportioned after a proper survey which may reveal that 30% of such salary should be apportioned to one department and 70% to the other department. The cost of lighting, when not metered, may similarly be apportioned on a survey of the number and wattage of light points and the hours of use in each cost centre.

The Departmental Trading, Profit and Loss Account

Draw the departmental trading, profit and loss account

Departmental Trading and Profit and Loss Account:

When the books and accounts are maintained on a columnar basis, Trading and Profit and Loss Account can also be prepared on columnar basis. There arises no difficulty in finding out gross profit and net profit for each department separately. From the analytical ledger accounts and subsidiary books department-wise figures are readily available. If an item of expenses definitely identified with a particular department, it can be termed as direct expenses with reference to the department.

For instance, salary of Manager and salesman of a particular department, special advertising, separately metered electricity etc. are expenses and exclusively meant for and identified with particular departments. Apart from this, there are some expenses termed as indirect expenses.

Certain types of expenses are not readily identifiable departmentally and the benefit of such type of expenses goes to all departments. And such types of expenses, called joint expenses, are incurred for the business as a whole.

For instance, rent, depreciation, selling expenses, welfare expenses, advertising etc. Allocation of such expenses among the various departments becomes indispensable on an equitable basis at the date of account. The important point in such cases is to fix the basis on which the different revenueitems are to be split up. It is neither possible nor desirable to sub-divide all items on equal basis.

Allocation of Common Expenses:

Normally, all direct expenses are charged to the respective departments, in case of indirect or general expenses, proper allocation among the departments must be made in order to ascertain the profit and loss made by each department. Each department is charged with proper business expenses. If the basis for such allocation is not specially mentioned, then the following procedure may be followed.

Some expenses cannot be apportioned and no basis of apportionment is practicable. For instance, interest on Loan, Income Tax, Salary to General Manager, Share Transfer expenses, Bank charges, Audit fees etc. Here these expenses can safely be transferred to General Profit and Loss Account.

Similarly, income of general nature such as Interest on Calls-in-arrears, Interest on Investment, fees on share transfer etc. credited to General Profit and Loss Account. The Departmental Trading Account shows the Gross Profit or Loss and Departmental Profit and Loss Account shows the Net Profit or Loss earned or suffered by each department.

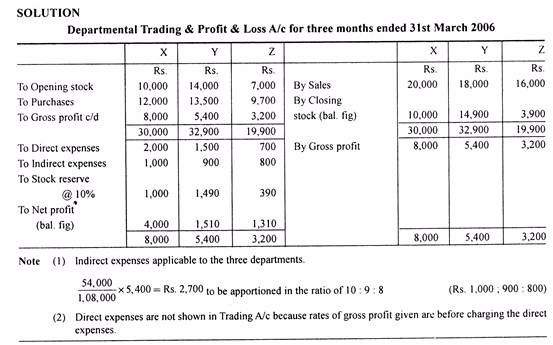

Example 1

Illustration 1:

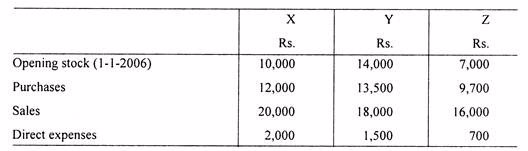

The proprietor of a large retail store wished to ascertain approximately the net profit of the X, Y and Z departments separately for the three months ended 31st March 2006. It is found impracticable actually to take stock on that date, but an adequate system of departmental accounting is in use, and the normal rates of gross profit for the three departments concerned are respectively 40%, 30% and 20% on turnover before charging the direct expenses. The indirect expenses are charged in proportion to departmental turnover.

The following are the figures for the departments:

The total indirect expenses for the period (including those relating to other departments) were Rs. 5,400 on the total turnover of Rs. 1, 08,000. Prepare a statement showing the approximate net profit, making a stock reserve of 10% for each department on the estimated value on 31-3-2006

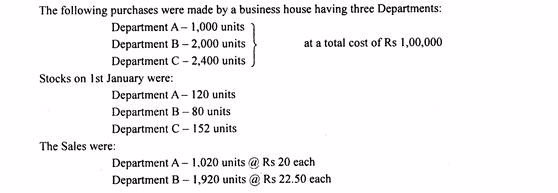

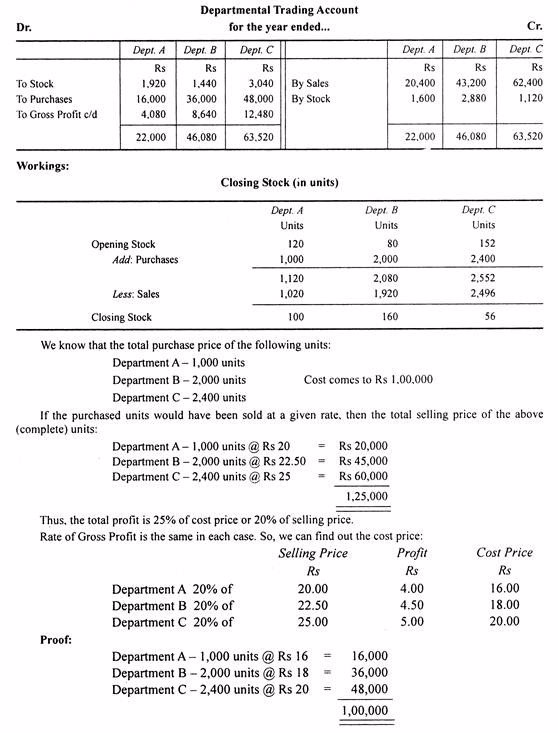

Example 2

Illustration 3:

Department C – 2,496 units @ Rs 25 each

The rate of Gross Profit is the same in each case. Prepare Departmental Trading Account.

Solution:

Inter-Departmental Transfers:

Goods are often supplied from one Department to another – Inter-Departmental transfer. Such transfer must be credited to Supplying Department and debited to Receiving Department. If the transfers are made at cost price, then it can be treated as mere transfer. No further adjustment is needed.

However, if the transfers of goods are made at selling price, then a profit is earned by the supplying department of the same organisation. When the goods, transferred from one department to another, still remain unsold with the transferee department, at the end of the accounting period, there arises a necessity to eliminate the unrealised profit on such stock on hand. This is because, so much of issuing department’s profit (notional) remain unrealised from the viewpoint of the firm as a whole. The reserve will be equal to the profit included in respect of unsold goods at the end of closing.

The entry is:

General Profit and Loss Account Dr.

To Stock Reserve

In certain cases, the transferee department may have some stock in the beginning of the accounting period, against which stock reserve was already created in the previous year, will also be transferred to General Profit and Loss Account by means of Journal entry:

Stock Reserve Account Dr.

To General Profit and Loss Account

Alternatively, a single journal entry can be passed for the unrealised profit on the basis of the difference between unrealised profit included in opening and closing stock.

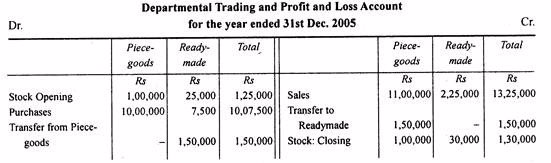

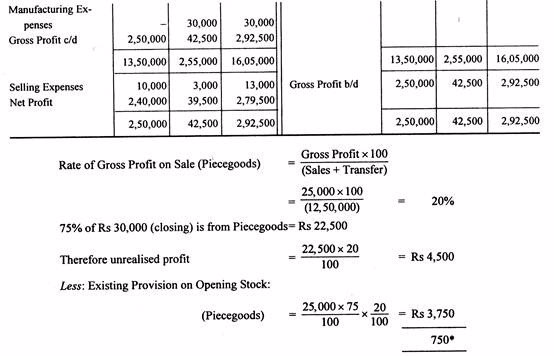

Example 3

Illustration 1:

A firm has two departments — Piece goods and readymade dresses. All goods purchased by the readymade department from Piece goods department are charged at the usual selling price.

From the following particulars prepare departmental trading and profit and loss accounts for the year ended Dec. 31, 2005:

The stocks in the readymade department are considered as consisting of 75% cloth supplied from Piece goods dept. and 25% expenses and cloths from outside. The Piece goods department earned gross profit in 2004 at the same rate as in 2005. General expenses of the business as a whole in 2005 amounted to Rs 45,000.

Solution:

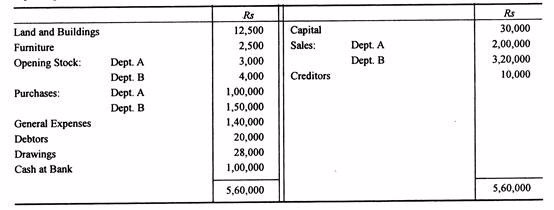

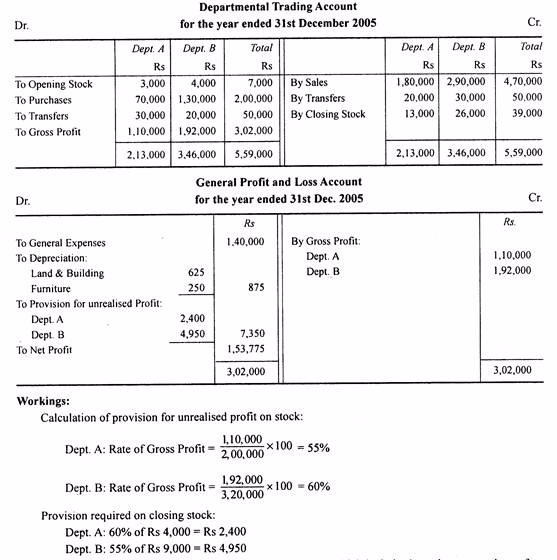

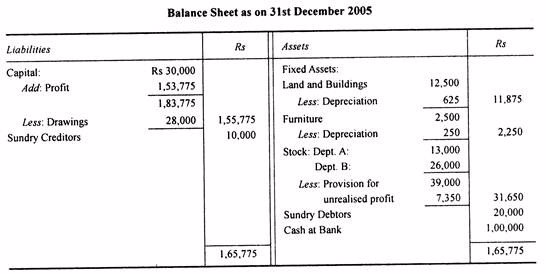

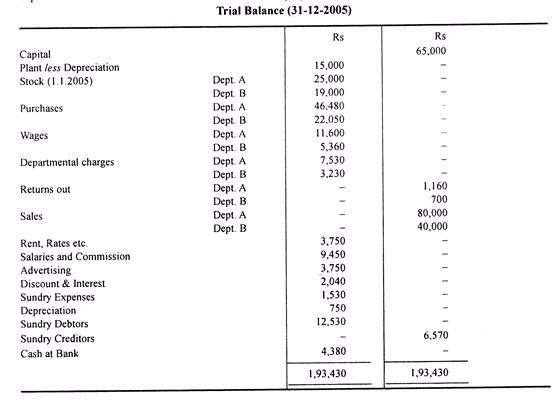

Example 4

Illustration 2:

From the following balances extracted from the books of a firm, prepare Departmental Trading and General Profit and Loss Account for the year ended 31st December 2005 and a Balance Sheet as on that date after adjusting the unrealised departmental profits, if any.

Additional information:

- Closing stock of Dept. A – Rs 13,000 including goods from Dept. B Rs 4,000 at cost to Dept. A.

- Closing stock of Dept. B – Rs 26,000-including goods from Dept. ARs 9,000 at cost to Dept. B.

- Sales Dept. A includes transfer of goods to Dept. B of the value of Rs 20,000 and sales of Dept. B includes transfer of goods to Dept. A of the value of Rs 30,000 both at market price to transferor departments.

- Opening stock of Dept. A and Dept. B includes goods to the value of Rs 1,000 and Rs 1,500 taken from Dept. B and Dept. A respectively at cost price to transferor departments.

- Depreciate land and buildings by 5% and furniture by 10% p.a.

Solution:

N.B. There is no need for any adjustment for opening stock which includes inter-departmental transfers. This is because goods have been valued at cost to the transferor department and not to transferee departments.

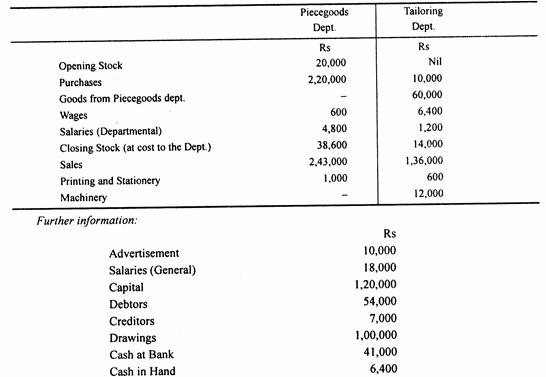

Exercise 1

EXCERSISE:

A company has two departments viz. Piece goods and Tailoring. All goods purchased by the Tailoring Department from Piece goods Department are sold at normal market prices, same as prices charged to outside customers.

From the following particulars prepare Departmental Trading and Profit and Loss Account and a Balance Sheet as on 31st March 2005.

A Department Balance Sheet

Draw a department balance sheet

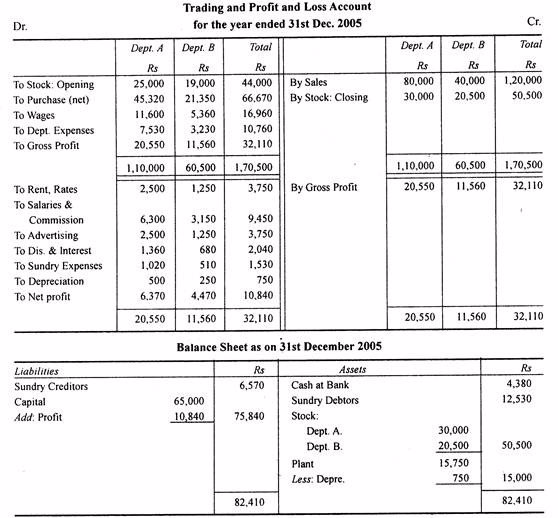

Example 5

Illustration 2:

From the following particulars you are required to prepare Trading and Profit and Loss Accounts for the year ended 31st December 2005, showing the gross and net profits of each department. Apportion the general expenses of the business on the basis of turnover. Also prepare the Balance Sheet.

Stock in hand Dec. 31, 2005 Dept. A Rs 30.000 and B Rs 20,500.

Total sales are Rs 1.20.000 i.e., Dept. A Rs 80.000 and B Rs 40.000. Proportion of general or indirect expenses chargeable to A 2/3 and B 1/3. (B.Com. Madurai. MS. Bharathiar)

Solution:

EmoticonEmoticon