Join Our Groups

TOPIC 2: PRINCIPLES OF DOUBLE ENTRY SYSTEM

In these concept, you are going to explore more about business transactions. It is very important that, you understand about the basic principles of double entry system. Please watch the following video and remember to share your ideas on the discussion forum.

Please use a regular YouTube link.

Description of a Business Transaction

Describe what a business transaction is

Exercise 1

Do you know what steps to take when recording any business transaction? Here is the summarized accounting cycle

An accounting transaction is a business event having a monetary impact on the financial statements of a business. It is recorded in the accounting records of the business. Examples of accounting transactions are:

- Sale in cash to a customer, this is like when you go to shop and buy goods in exchange for money.

- Sale on credit to a customer. Credit salesare allowances of goods to customers in order to pay in advance.The name speaks for itself. It is goods given to a customer oncredit, meaning that you sell the goods and collect cash at a later date per agreement with customer

- Receive cash in payment of an invoice owed by a customer. This is mostly used consultations nowadays. example, some one may be working to provide her skills on a project and she wrote an invoice to ask for payment after the end of the project. Import and exports use this kind of transaction too.

- Purchase fixed assets from a supplier

- Record the depreciation of a fixed asset over time

- Purchase consumable supplies from a supplier

- Investment in another business

- Investment in marketable securities

- Engaging in a hedge to mitigate the effects of an unfavorable price change

- Borrow funds from a lender

- Issue a dividend to investors

- Sale of assets to a third party

Analysis of a Business Transaction

Analyses a business transaction

What’s the difference between a cash and credit transaction?The only difference between cash and credit transaction is the timing of the payment.

- Transactions are the building blocks of our accounts. Any transactions that occur within our business should be present in our accounting records.

- There are many different types of transactions to keep track of such as sales, purchases, and even more. A regular point of confusion that we come across when we talk to small businesses about their accounts is the difference between cash and credit transactions. So, what is the difference?

- The only difference between cash and credit transactions is the timing of the payment. A cash transaction is a transaction where payment is settled immediately. On the other hand, payment for a credit transaction is settled at a later date.

- Try not to think about cash and credit transactions in terms of how they were paid, but rather, when they were paid. For example, you may buy some groceries at your local shop and pay for them in cash there and then, that’s a cash transaction. However, what if you paid by card rather than cash? That can also be classified as a cash transaction because you paid immediately.

- On the other hand, credit transactions are paid at a later date than when the exchange of goods or services took place and almost all of time an invoice for the transaction is issued. The time period before payment can vary depending on the types of businesses or even the industry in which the transaction is taking place. Once again, when payment is finally settled for the invoice, it may be done with cash or card, or any other payment method but it is still a credit transaction.

- Businesses will have a mixture of cash and credit transactions make up their accounting records. Some businesses may have the majority of their transactions be either one or the other and some will have a more even split. However, you would be hard pressed to find a business that didn’t have at least one cash or credit transaction occur during its lifetime.

- Along with whether a transaction is classified as cash or credit another category is used to classify basic accounting transactions. We also need to know whether or not it is a sale, purchase or payment. This gives us a list of basic transactions:

- 1. Cash sale

- Some of these, like cash and credit sales as well as credit purchases are more common that the others but depending on what type of transaction we have, we can find a home for it in our accounts.

Changing Values of Things Owned and Owed

Sort the changing values of things owned and owed

Accounting standards define an asset as something your company owns that can provide future economic benefits. Cash, inventory, accounts receivable, land, buildings, equipment, these are examples of company's assets.Liabilities are your company's obligations, either money that must be paid or services that must be performed. Example of liabilities include company loan, the money used to pay rent. You should be aware that assets increases company's net worth while liabilities does the opposite.

Assets

Assets refer to resources owned and controlled by the entity as a result of past transactions and events, from which future economic benefits are expected to flow to the entity. In simple terms, assets are properties or rights owned by the business. They may be classified as current or non-current.

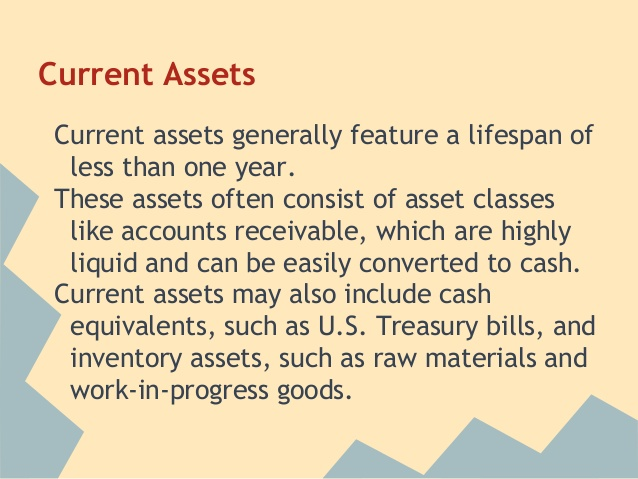

A. Current assets – Assets are considered current if they are held for the purpose of being traded, expected to be realized or consumed within twelve months after the end of the period or its normal operating cycle (whichever is longer), or if it is cash. Examples of current asset accounts are:

- Cash and Cash Equivalents – bills, coins, funds for current purposes, checks, cash in bank, etc.

- Receivables – Accounts Receivable (receivable from customers), Notes Receivable (receivables supported by promissory notes), Rent Receivable, Interest Receivable, Due from Employees (or Advances to Employees), and other claims

- Inventories – assets held for sale in the ordinary course of business

- Prepaid expenses – expenses paid in advance, such as, Prepaid Rent, Prepaid Insurance, Prepaid Advertising, and Office Supplies

• Allowance for Doubtful Accounts – This is a valuation account which shows the estimated uncollectible amount of accounts receivable. It is a contra-asset account and is presented as a deduction to the related asset – accounts receivable.

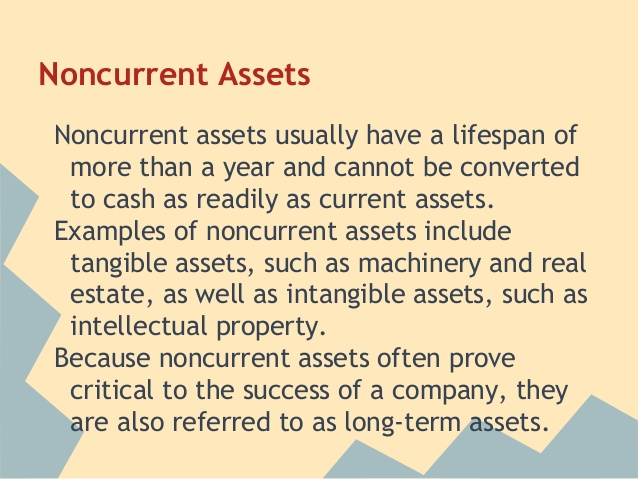

B. Non-current assets – Assets that do not meet the criteria to be classified as current. Hence, they are long-term in nature – useful for a period longer that 12 months or the company's normal operating cycle. Examples of non-current asset accounts include:

- Long-term investments – investments for long-term purposes such as investment in stocks, bonds, and properties; and funds set up for long-term purposes

- Land – land area owned for business operations (not for sale)

- Building – such as office building, factory, warehouse, or store

- Equipment – Machinery, Furniture and Fixtures (shelves, tables, chairs, etc.), Office Equipment, Computer Equipment, Delivery Equipment, and others

- Intangibles – long-term assets with no physical substance, such as goodwill, patent, copyright, trademark, etc.

- Other long-term assets

• Accumulated Depreciation – This is a valuation account which represents the decrease in value of a fixed asset due to continued use, wear & tear, passage of time, and obsolescence. It is a contra-asset account and is presented as a deduction to the related fixed asset.

Liabilities

Liabilities are economic obligations or payables of the business.

Company assets come from 2 major sources – borrowings from lenders or creditors, and contributions by the owners. The first refers to liabilities; the second to capital.

Liabilities represent claims by other parties aside from the owners against the assets of a company.

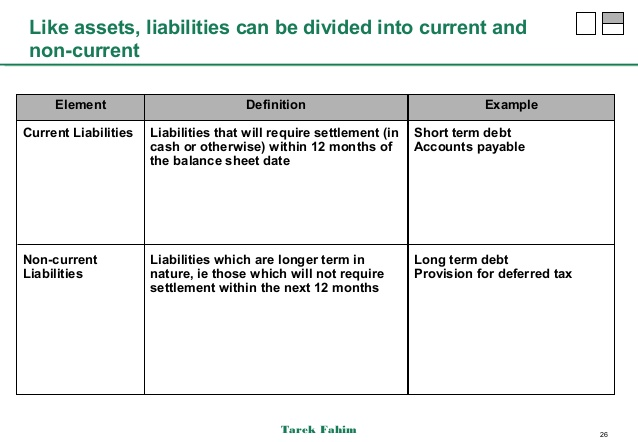

Like assets, liabilities may be classified as either current or non-current.

A. Current liabilities – A liability is considered current if it is due within 12 months after the end of the balance sheet date. In other words, they are expected to be paid in the next year.

If the company's normal operating cycle is longer than 12 months, a liability is considered current if it is due within the operating cycle.

Current liabilities include:

- Trade and other payables – such as Accounts Payable, Notes Payable, Interest Payable, Rent Payable, Accrued Expenses, etc.

- Current provisions – estimated short-term liabilities that are probable and can be measured reliably

- Short-term borrowings – financing arrangements, credit arrangements or loans that are short-term in nature

- Current tax liabilities – taxes for the period and are currently payable

- Current-portion of a long-term liability – the portion of a long-term borrowing that is currently due.

Example: For long-term loans that are to be paid in annual installments, the portion to be paid next year is considered current liability; the rest, non-current.

B. Non-current liabilities – Liabilities are considered non-current if they are not currently payable, i.e. they are not due within the next 12 months after the end of the accounting period or the company's normal operating cycle, whichever is shorter.

In other words, non-current liabilities are those that do not meet the criteria to be considered current. Hah! Make sense? Non-current liabilities include:

- Long-term notes, bonds, and mortgage payables;

- Deferred tax liabilities; and

- Other long-term obligations

Account Balances

Determine account balances

Capital

Also known as net assets or equity, capital refers to what is left to the owners after all liabilities are settled. Simply stated, capital is equal to total assets minus total liabilities. Capital is affected by the following:

- Initial and additional contributions of owner/s (investments),

- Withdrawals made by owner/s (dividends for corporations),

- Income, and

- Expenses.

Owner contributions and income increase capital. Withdrawals and expenses decrease it.

The terms used to refer to a company's capital portion varies according to the form of ownership. In a sole proprietorship business, the capital is called Owner's Equity or Owner's Capital; in partnerships, it is called Partners' Equity or Partners' Capital; and in corporations, Stockholders' Equity.

In addition to the three elements mentioned above, there are two items that are also considered as key elements in accounting. They are income and expense. Nonetheless, these items are ultimately included as part of capital.

Income

Incomerefers to an increase in economic benefit during the accounting period in the form of an increase in asset or a decrease in liability that results in increase in equity, other than contribution from owners.

Income encompasses revenues and gains.

Revenues refer to the amounts earned from the company’s ordinary course of business such as professional fees or service revenue for service companies and sales for merchandising and manufacturing concerns

Gains come from other activities, such as gain on sale of equipment, gain on sale of short-term investments, and other gains.

Income is measured every period and is ultimately included in the capital account. Examples of income accounts are: Service Revenue, Professional Fees, Rent Income, Commission Income, Interest Income, Royalty Income, and Sales.

Expense

Expenses are decreases in economic benefit during the accounting period in the form of a decrease in asset or an increase in liability that result in decrease in equity, other than distribution to owners.

Expenses include ordinary expenses such as Cost of Sales, Advertising Expense, Rent Expense, Salaries Expense, Income Tax, Repairs Expense, etc.; and losses such as Loss from Fire, Typhoon Loss, and Loss fromTheft. Like income, expenses are also measured every period and then closed as part of capital.

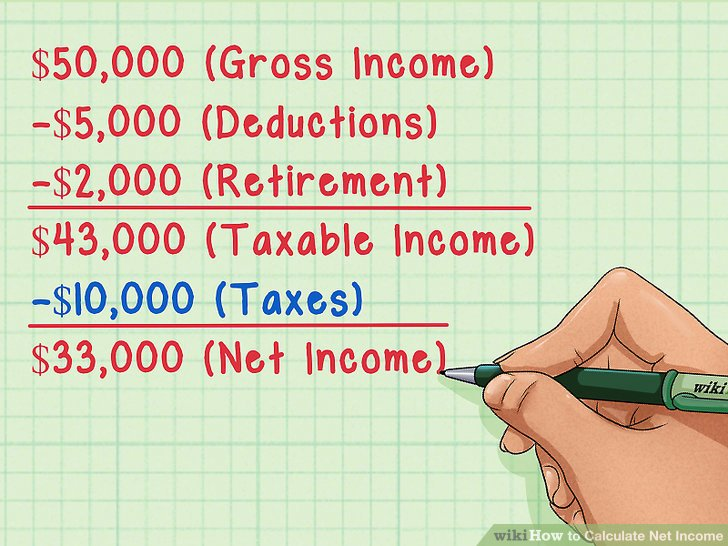

Net income refers to all income minus all expenses. See below to see how net income is calculated from gross income. For the employees this is also known as take home.

EmoticonEmoticon