Join Our Groups

TOPIC 6: ELEMENTARY TRADING PROFIT AND LOSS ACCOUNTS

Final accounts give a concise idea about the profitability and financial position of a business to its management, owners, and other interested parties. All business transactions are first recorded in a journal. They are then transferred to a ledger and balanced.

These final tallies are prepared for a specific period. The final accounts consist of trading account, profit and loss account, and balance sheet.

Trading, Profit and Loss Account

Describe what a Trading, profit and Loss account is

Trading account are those accounts prepared at the end of accounting period for the determination of gross profit or gross loss of the business.

GROSS PROFIT=SALES-COST OF GOODS SOLD

PROFIT AND LOSS ACCOUNT;

A profit and loss statement (P&L) is a financial statement that summarizes the revenues, costs and expenses incurred during a specific period of time, usually a fiscal quarter or year. These records provide information about a company's ability –or lack thereof –to generate profit by increasing revenue, reducing costs, or both. The P&L statement is also referred to as "statement of profit and loss", "income statement," "statement of operations," "statement of financial results," and "income and expense statement."

NET PROFT=NET PROFIT & OTHER INCOME-TOTAL EXPENSES.

EXAMPLE

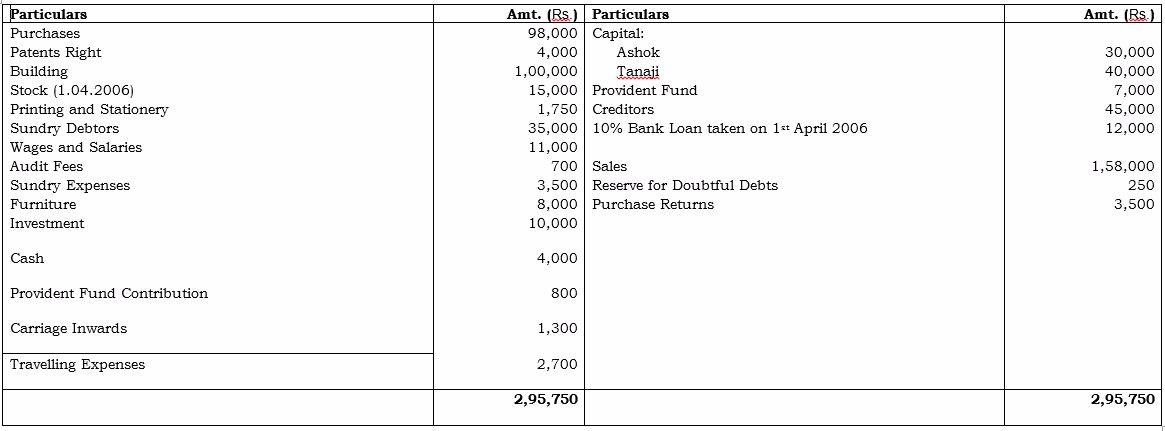

Ashok and Tanaji are Partners sharing Profit and Losses in the ratio 2:3 respectively. Their Trial Balance as on 31st March, 2007 is given below. You are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2007 and Balance Sheet as on that date after taking into account the given adjustments.

Trial Balance as on 31st March, 2007

Adjustments:

- Closing stock is valued at the cost of Rs. 15,000 while its market price is Rs.18,000.

- On 31st March, 2007 the stock of stationery was Rs. 500.

- Provide reserve for bad and doubtful debts at 5% on debtors.

- Depreciate building at 5% and patent rights at 10%.

- Interest on capitals is to be provided at 5% p.a

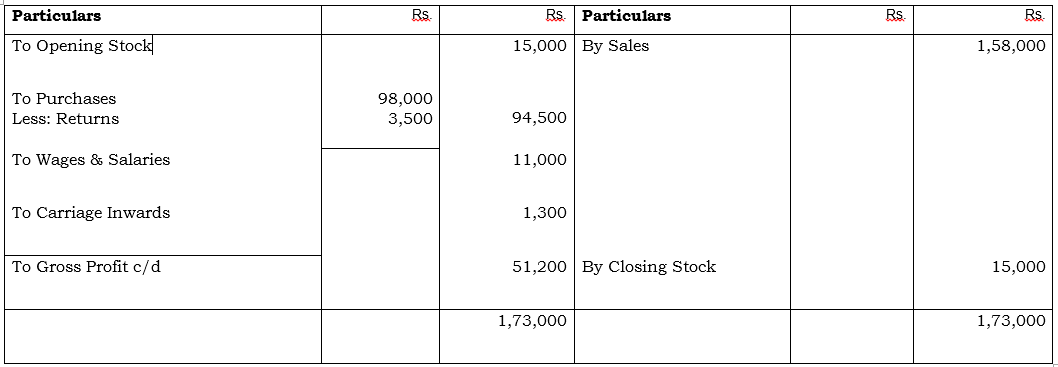

Trading Account for the year ended 31st March 2007

Gross Profit or Gross Loss

Determine the Gross profit or Gross Loss

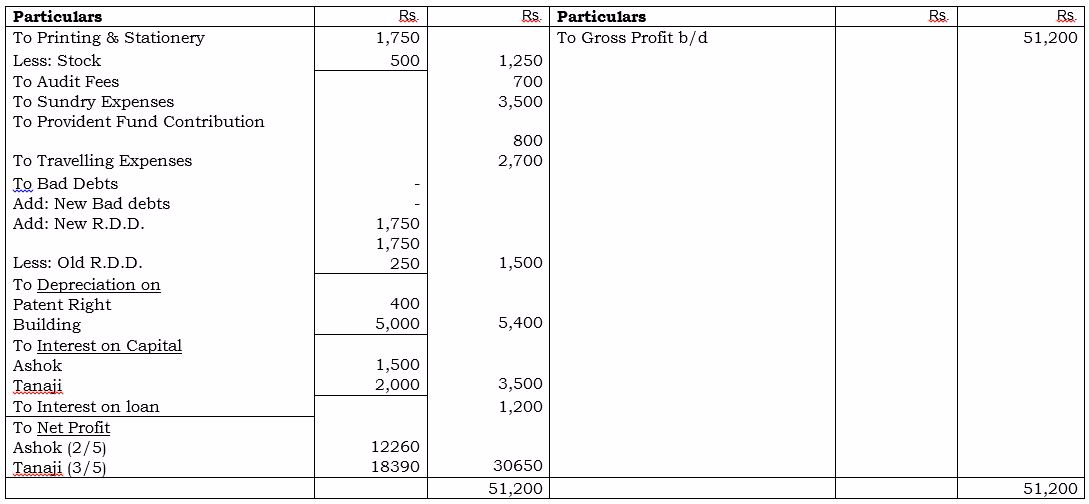

Profit & Loss A/c for the year ended 31st March 2007

Partner’s Capital A/c

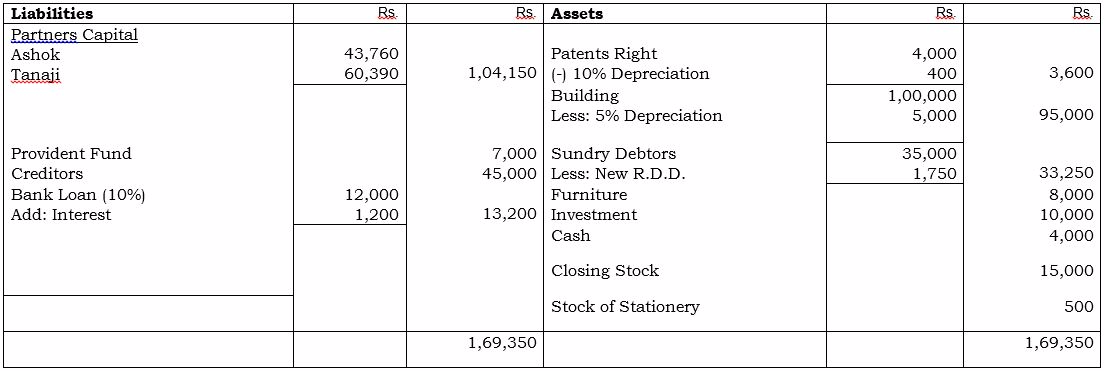

Balance Sheet as on 31-3-2007

EmoticonEmoticon